We use Cookies

We use cookies to enhance your experience and analyse traffic. By clicking "Accept All" you consent to our use of cookies.

We use Cookies

We use cookies to enhance your experience and analyse traffic. By clicking "Accept All" you consent to our use of cookies.

Real-world stablecoin payments volume doubled in 2025 to roughly $400 billion, and about 60 percent of that flow was business-to-business, according to Bessemer Venture Partners.

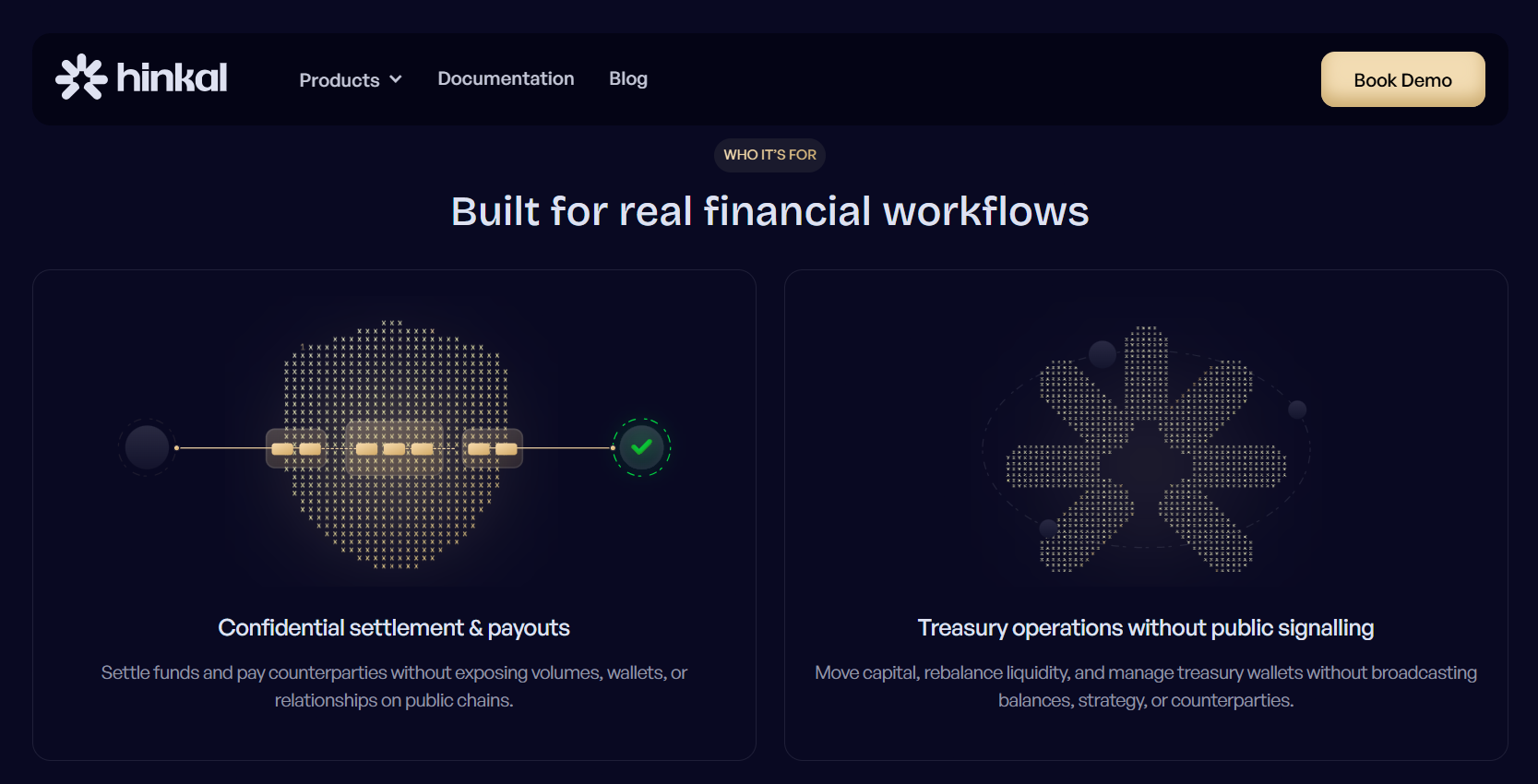

Hinkal gives fintechs the fastest way to add confidential stablecoin settlement to the stack they already run, through a single API or SDK, with no change to their chains, wallets, or custody.

Yet almost all of that volume settles on public blockchains that broadcast every counterparty, amount, payout, and treasury movement in plain sight, which for a regulated payment business is a structural blocker rather than a minor inconvenience.

This guide ranks the best crypto payment APIs with private settlements for fintechs in 2026, explains the criteria used to score them, and shows exactly where each option fits.

[[KEY_TAKEAWAYS]]

Public blockchains were built to be transparent, and that transparency is exactly what makes them hard to use for regulated payments. When a payment service provider settles a merchant, when a payroll platform pays a workforce, or when an exchange processes a withdrawal, the destination wallet, the amount, and the relationship behind the transfer are all visible to anyone watching the chain.

Competitors can map merchant volumes, counterparties can reverse-engineer pricing, and treasury movements telegraph strategy to the entire market.

For the businesses driving stablecoin adoption, this is not a theoretical concern. Custodians, institutional and embedded wallet providers, payroll platforms, merchants, PSPs, iGaming operators, exchanges, on-ramps, stablecoin card providers, and fintechs all handle sensitive flows that should not be public by default.

They also cannot simply move to a private chain, because their liquidity, their stablecoins, and their users already live on Ethereum, Solana, TRON, and the major EVM networks. What they need is a way to keep settlement confidential on the rails they already use, without breaking custody or compliance. That is the exact gap a private-settlement payment API is meant to close.

Private settlement does not change how a fintech moves money, only what the public ledger can see. Funds enter a private balance held inside the Hinkal smart contract and controlled by the business's existing wallet keys, and from there they can move in four ways depending on the flow:

Because zero-knowledge proofs validate each of these transfers, every transaction is provably correct on the public chain even though the participants and amounts stay private. That is what lets a payment team settle, pay out, or receive confidentially without asking counterparties to change anything about how they operate.

Not every privacy tool is a fit for fintech settlement, so this ranking scores each option against the requirements a payment team actually has to meet:

The ranking below reflects how each provider performs against those criteria for a fintech that wants private stablecoin settlement without rebuilding its stack.

Hinkal Integrations is the API and SDK layer of Hinkal, a privacy protocol that adds confidential settlement directly on the public chains a fintech company already operates on.

Instead of routing wallet-to-wallet, a business executes transactions from a private balance held inside the Hinkal smart contract and controlled by its existing wallet keys, so on-chain observers see only the contract and a relayer address while the sender, recipient, and amount stay private.

Every transaction is verified with zero-knowledge proofs, screened by Chainalysis KYT before it executes, and auditable through scoped viewing keys. What sets it apart for fintechs is the combination of full privacy and practical reach: it is the only solution here that keeps sender, recipient, and amount confidential across EVM, Solana, and TRON at once, and it exposes that capability as a language-agnostic API and a frontend SDK, so a wallet or payment product can offer a private balance next to the regular balance and a private send next to the regular send.

It is non-custodial, has processed more than $500 million in cumulative volume across roughly three and a half years in production, has completed six security audits, and pairs teams with a forward-deployed engineer for integration. That track record is backed by investors including Draper Associates, SALT, SNZ Capital, and NGC Ventures, with early incubation at Stanford and through Binance's MVB program.

For businesses running settlement at scale, Hinkal Prime layers on permissioned multi-user access, pending and batch payouts, and controls on high-value transactions, while Hinkal Pay covers teams that want confidential settlement without building. Enterprise settlement runs at a transparent 0.10% per transaction.

Pros

Cons

Zama is a strong and genuinely differentiated confidentiality layer that uses fully homomorphic encryption to keep balances and amounts encrypted end to end, including while they are being processed, and it went live on Ethereum mainnet at the end of December 2025 with real deployments such as encrypted payroll and banking-style apps.

It is chain-agnostic in design and backed by a well-capitalized team, which makes it a credible foundation for confidential on-chain finance. The distinction for a fintech is that Zama is infrastructure to build confidential applications on, not a turnkey payment API that a settlement team can call out of the box, and its multichain footprint is still expanding, with Solana support slated for the second half of 2026 and no native TRON path.

Hinkal, by contrast, is already a working settlement API across EVM, Solana, and TRON today, which is why it leads for teams that need private payouts now rather than a platform to build them on.

Pros

Cons

Canton is the most institutionally adopted name on this list, and for good reason: it is a privacy-enabled blockchain purpose-built for regulated finance, with atomic settlement and selective data visibility that let counterparties transact without exposing full positions to each other.

Its roster is heavyweight, including JPMorgan, Goldman Sachs, DTCC, and Broadridge, with Visa joining in March 2026 as the first payments company to serve as a Super Validator. That credibility is real.

The trade-off for a fintech is that Canton is a separate network to adopt and integrate with, not a smart contract on the public chains the fintech already uses, and its center of gravity is capital markets and tokenized assets rather than everyday stablecoin payment and payout flows.

Hinkal takes the opposite approach by adding confidentiality on Ethereum, Solana, TRON, and the EVM networks a fintech company is already on, with a lighter integration that a lean product team can ship.

Pros

Cons

Railgun is a mature and well-regarded privacy system that shields sender, recipient, token, and amount using zero-knowledge proofs, and it ships a developer SDK, viewing keys, and Private Proofs of Innocence for compliance-friendly disclosure.

It has recorded billions of dollars in cumulative shielded volume and offers deep DeFi composability, which makes it a capable option for privacy-conscious on-chain activity. Notably, it shares architectural DNA with Hinkal, using Groth16 proofs and UTXO-style commitments with a relayer that broadcasts transactions.

The difference that matters for fintech settlement is scope and reach: Railgun is EVM-only, with no native Solana or TRON support, and it is built primarily for individual DeFi users shielding their activity rather than for business settlement with batch payouts and team controls.

Hinkal covers the broader multichain settlement surface and is designed around business flows, from Hinkal Prime team permissions to confidential batch payouts.

Pros

Cons

Inco is a confidentiality layer that uses fully homomorphic encryption to keep data encrypted even during computation, with a modular design meant to add confidentiality to existing chains rather than replace them. It is a capable primitive for builders who want to explore encrypted application logic.

The reason it sits lower for fintech payments is that it is a confidentiality primitive for developers, not a ready payment or settlement API, and it is earlier in its production journey than solutions with years of settlement uptime.

A fintech that wants a working private payout flow would still have to build the payment product on top. Hinkal delivers that settlement layer as a finished, callable surface with a multi-year production record.

Pros

Cons

The right choice comes down to the flows you settle and the stack you already run. Here is how the options map to the most common fintech use cases:

For the majority of fintechs that settle stablecoins across EVM, Solana, and TRON and want privacy without rebuilding their stack, Hinkal Integrations is the most direct path, because it pairs full confidentiality with non-custodial control and a drop-in API and SDK.

The other options fit narrower cases, whether that is building confidentiality primitives from scratch or running institutional capital-markets flows, but they ask a payment team to either build more or migrate further.

Hinkal Integrations is the strongest crypto payment API for fintechs that need private settlements in 2026, because it delivers full confidentiality across the chains those businesses already use without touching their custody or compliance.

As stablecoin payments scale into the hundreds of billions and privacy shifts from a nice-to-have to an operating requirement, the winning approach is not a new network to migrate to but a private balance and a private send embedded under the products fintechs already run.

If you are evaluating how to add confidential stablecoin settlement to your stack, book a demo with the Hinkal team to see it working on your rails.

Read Next:

The best crypto payment API for fintechs with private settlements in 2026 is Hinkal Integrations, because it keeps sender, recipient, and amount private across EVM, Solana, and TRON, stays non-custodial, and drops into an existing product through an API or SDK while preserving compliance controls.

Private settlements on a public blockchain work by moving funds into a private balance held inside a smart contract and controlled by the user's existing wallet keys, then executing transfers that zero-knowledge proofs verify as valid while keeping the sender, recipient, and amount hidden from public observers.

Hinkal supports private settlements across Ethereum, Polygon, Arbitrum, Optimism, Base, Solana, TRON, Arc, and Tempo, covering EVM, Solana, and TRON from a single integration, with cross-chain movement that preserves privacy.

Private crypto settlements are compliant for fintechs when privacy applies to the public ledger rather than to auditors, which is how Hinkal operates through Chainalysis KYT screening before every transaction, scoped and revocable viewing keys for selective disclosure, and downloadable transaction history for regulators and counterparties.

Yes, Hinkal Integrations is non-custodial, meaning Hinkal never holds a fintech's funds or keys, and the private balance is controlled entirely by the same wallet keys the business already uses to sign its transactions.

.webp)